The distance sale plays an increasingly important role in economic turnover. Its popularity among entrepreneurs results from the possibility of the reduction of fixed costs arising from the maintenance of stationery stores while increasing the extent of potential consumers. During the lockdown introduced due to the prevailing COVID-19 pandemic, the distance sale saved a significant part of Companies from a crisis or from the termination of their business. This experience has shown the enormous potential for online shopping.

Nevertheless, due to the specific nature of the VAT regulations regarding the distance selling where a purchaser is an individual person, the execution of the VAT settlement correctly can be questionable.

→What is distance selling?

According to the EU VAT Directive, two types are distinguished:

1) the distance selling from the territory of the country – it means that the delivery of goods transported by the VAT taxpayer or on its behalf takes place from the territory of the country of origin to the other Member States’ territory which is a country of destination of shipped or transported goods.

2) the distance selling on the territory of the country – it means that the delivery of goods transported by the VAT taxpayer or on its behalf takes place from the territory of other Member States to the territory of the country which is a country of destination of shipped or transported goods.

→VAT liability

Based on the general rules the tax liability has arisen in the moment of delivery of goods unless the payment is made before shipment of goods.

→Place of taxation

The main rule establishes the place of taxation is the country of the purchaser.

In the case of distance selling from the territory of the country the place of taxation is a country of supplier, against the general rule. That solution has been introduced for the purpose of simplification of transactions settlement performed between EU countries. Therefore, the supplier makes a VAT settlement from performed transactions in the country from where the goods are shipped following applying the prevailing VAT rates, before exceeding the distance selling threshold established by the EU country of destination.

To be able to use the preferential option, the entrepreneur must fulfill the following requirements:

- a taxpayer must collect shipment documents before the deadline for submitting a VAT declaration for a given settling period from the carrier responsible for the transport of goods,

- a taxpayer must receive a confirmation of receipt by purchaser outside the territory of the country, before the deadline to submitting the VAT declaration for that settling period.

Important!

The taxpayer has a right to use a preferential option of taxing the supply of goods on the territory of the country of delivery. However it may be used by entities whose total value of goods other than excise goods shipped or transported to the same Member State within distance selling from the territory of the country did not exceed the amount expressed in the previous tax year with the reduction of the tax amount, by the Member State of destination for shipped or transported goods. The notification about choosing an option is submitted to the tax authorities in the country when the delivery starts, at least 30 days before the shipment for which the taxpayer wishes to use the option.

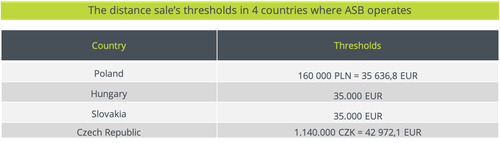

→ Thresholds

Entrepreneurs who perform transactions classified as a distance sale are obligated to control the value of delivered goods.

It is important, especially for entrepreneurs that have high-value goods, and reaching the threshold is really likely.

If the indicated limits are exceeded, the distance selling must be taxed in the country of destination.

Reaching the thresholds is associated with the obligation of registration for VAT purposes in a specific country, switching to the arrival country’s VAT rate, and submitting the VAT declarations in other Member State.

! As of July 2021 new rules of reporting distance selling and One-Stop-Shop (OSS) VAT return will be implemented by the Member States. More details in this matter will follow soon.

Anna Szafraniec

CEE VAT Compliance Director

E: aszafraniec@asbgroup.eu

Łukasz Woźniak

VAT Compliance Manager

E: lwozniak@asbgroup.eu