The president has signed off several laws bringing important changes from next year. We map them out in this article.

Cancellation of the ceiling on the monthly tax bonus

From the New Year, the maximum limit for the payment of the monthly tax bonus, i.e. the difference between calculated income tax and the child allowance paid out by the tax office in the event of a negative tax liability, will in effect be abolished.

The limit of the monthly bonus has to date been CZK 5,025.

Higher discount per taxpayer

The annual discount per taxpayer increases to CZK 30,840 in 2022.

Change in the solidarity tax amount

Last year, progressive tax rates of 15% and 23% were approved, thus abolishing the solidarity surcharge; the 23% tax rate will be applied in 2022 to that part of the tax base exceeding 48 times the average wage (CZK 155,644 per month, CZK 1,867,728 per year).

It remains the case that taxpayers whose income was subject to the solidarity surcharge, to whom the second, increased, tax rate of 23% will apply, will not have to file a tax return for this reason and may apply for annual settlement through their employer.

Application of discounts – threshold age (18 years, 26 years)

The age limit must be met as of the beginning of the month. In the case of a non-studying child reaching the age of 18 or a (higher education) student attaining 26 years during a month, it is possible to count the month during which the child/student attained that age. However, when a child is born on the first day of the month, the situation is different. Contrary to previous interpretations, the new Civil Code is now applied. According to the General Financial Directorate, a non-studying child attains the age of 18 on the first day of the month (similarly, a higher education student reaches the age of 26 on the first day of the month) and this condition is no longer met. The provision in Section 601(1) of the Civil Code provides that if a law is to come into force on a certain day, it will do so at the very beginning of that day. The child therefore reaches the age of 18 or 26 at midnight on the first day of the month, and for this month the right to tax relief expires.

Meal voucher lump sum

The amount of the meal allowance in 2022 will also affect employee catering. That is, if the employer decides to increase the employee benefit in the form of a cash contribution, the so-called meal voucher lump sum. For the employee the cash contribution per single shift is exempt from income tax (and thus from insurance deductions) up to 70% of the upper limit of the meal allowance for a business trip lasting 5 to 12 hours set for salary-paid employees, i.e. Those employees referred to in Section 109(3) of the Labour Code. For 2022, this will be CZK 82.60 (70% of CZK 118).

Minimum wage

The minimum wage for contracted working hours of 40 hours per week for 2021 is set at CZK 16,200 per month and CZK 96.40 per hour.

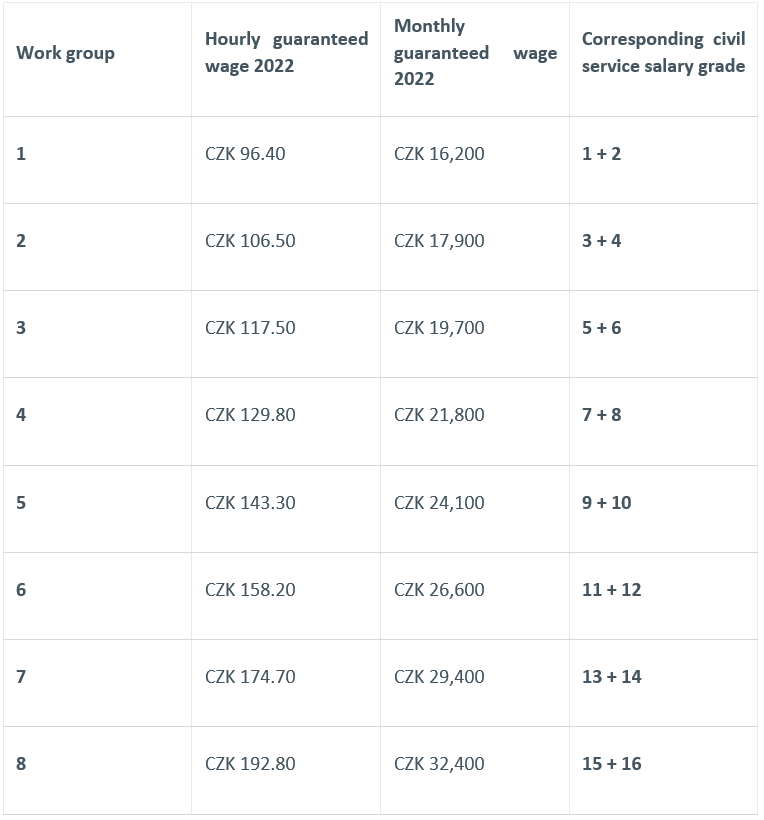

Guaranteed wage

Employees whose employment is not covered by a collective agreement are protected from the imposition of too low a salary by a "guaranteed wage". Work performed is graded according to its complexity, responsibility and strenuousness into eight individual groups, with a minimum level of guaranteed wage being set for each of them. Thus, not only is the minimum wage binding on employers, it must be provided at least at the level of the relevant groups of the lowest level of guaranteed wages. And this grows with each increase in the minimum wage.

Similar to the minimum wage, the lowest levels of the guaranteed wage are set both hourly and monthly, and similarly to a wage lower than the minimum wage, any wage lower than the guaranteed wage must be topped up. Wages or salaries for this purpose do not include wages or salaries for overtime working, pay for work on public holidays, night work, work in a difficult environment and work on Saturdays and Sundays. The lowest guaranteed wage levels do not apply to non-employment agreements.

Changes in sickness insurance

Long-term care allowance

Due to these changes, more people should have the long-term care allowance available to them in the future. According to Minister of Labour Jana Maláčová, there is a particular need to improve help for people who are in the closing stages of their lives, and it is in interests of everyone to be able to spend their time at home.

From the New Year, the right to the long-term care allowance will also arise in the situation where a patient has been resident in an inpatient care facility for at least four calendar days. At present, they must be there for at least 7 calendar days.

It still applies that the person being treated must be an individual whose serious health disorder has required hospitalization and who is expected to require at least one month's care at home after being released from hospital.

In the case of the terminally ill, the condition of hospitalization for the provision of the long-term care allowance will not apply if home care is possible. The annex specifies that these cases concern the terminally ill with poor prospects and a need for palliative care.

New conditions will also apply to the submission of an application for a decision on the need for long-term care due to a ruling on a long-term care allowance. Now there will be time for this up to 8 days following the end of hospitalization. At present, it is necessary to apply on the day of the end of hospitalization

Care allowance

From January, the standard care allowance will not only apply to people living in the same household.

Now relatives who care for a patient but do not live with him or her can also receive it. This will help most often in those situations where grandparents help to look after sick children or where it is necessary to take care of an elderly family member, but the care is not long-term.

The short-term care allowance can now be drawn down by:

- direct relatives (parents, grandparents, children, grandchildren, etc.),

- siblings (regardless of whether they have one or both parents in common),

- spouses and registered partners,

- parents of spouses or registered partners.

In addition to the benefit itself, close relatives will be able to take time off to care for a family member. But of course only if he/she is a participant in sickness insurance under employment or self-employment.

Paternal post-natal care

The amendment to the Sickness Insurance Act will also bring about a change for new fathers (or those who have taken into their care a child under the age of seven, thereby replacing parental care).

They will now be able to receive the paternal post-natal care (abbreviated to paternity) benefit for two weeks instead of one.

In fact, this change pre-emptively reflects one of the requirements of the European Directive on work-life balance, which the Czech Republic must implement in its legislation. The same document also acknowledges the right to paternity leave regardless of the time worked, the duration of the employment relationship or the personal or family status of the worker.

At the same time, the amendment will extend the period for which paternity benefit may be provided. But only in the situation where a new-born has been hospitalized during the first six weeks of life. In this case, the period is extended by the time the child has spent in hospital. This change will cover cases where a child is in an incubator, for example, or has had to stay in hospital longer for other reasons and the father does not come sufficiently into contact with him or her. He will now have the opportunity to take time off either during the first six weeks or when the mother is at home with the child.

Are you interested in how these legislative changes will specifically affect your company and your employees? Do not hesitate to contact us at any time.