The Ministry of Finance presented a draft bill introducing the new tax, referred to as advertising contribution. The tax will be imposed solely on particular types of activities - online advertising and traditional media business.

Advertising tax in Europe

By introducing this new charge Poland follows the example of a number of OECD and European Union countries that have already implemented similar solutions. Advertising contribution was implemented in France, Austria, Greece and Hungary. The contribution rate in Poland will not differ from the ones applied in other CEE countries and will depend on the type of advertised goods, medium category and the size of the broadcaster.

The planned advertising contribution is going to be applied to:

- Traditional advertising: on television, radio or an external medium (for example billboards), in the press or cinema;

- Internet advertising.

Entities obliged to pay the advertising contribution

The contribution for traditional advertising will be paid by media service providers, broadcasters, cinema operators, entities placing the advertisement on an external advertising medium and publishers whose revenues obtained from the service provided in Poland exceed the threshold of:

- PLN 1M - for broadcasting an advertisement on TV or radio, displaying an advertisement in a cinema or placing an advertisement on an external medium;

- PLN 15M - for placing an advertisement in the press.

The contribution for online advertising will be paid by service providers (digital services) who provide online advertising services in Poland, provided that they jointly meet the following conditions:

- the service provider's total revenues or the consolidated total revenues of the group of entities to which the service provider belongs, regardless of where they were obtained, in the financial year exceeded EUR 750M,

- the service provider's revenues or the consolidated revenues of the group of entities to which the service provider belongs, from the provision of internet advertising services Poland, in the financial year exceeded EUR 5M.

It is estimated that only entities with significant revenues from the online advertisement will be subject to the contribution. Internet advertising will be considered as rendered in Poland if its recipient stays in Poland. In order to determine this, it may be necessary to use e.g. the recipient's IP address or device geolocation.

Not only the entities with significant revenues (from the online advertisement) will be subject to the contribution, but it can be also real estate’s companies selling its commercial space for advertising.

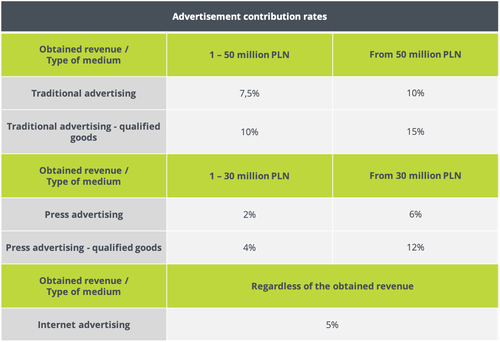

Advertisement contribution rates

In the case of traditional advertising, the contribution base will be calculated as the sum of advertisement revenues.

In the case of Internet advertising, the contribution base will be calculated as obtained revenue multiped by the percentage of the number of recipients located in Poland. Revenue should be understood as everything that constitutes the payment for advertising services less VAT. It means that the new contribution may cover, for example, compensation payments. The rates are planned as follows:

Higher rates will be used to revenues from advertising of goods harmful to health, in particular sweetened beverages, but also dietary supplements.

The contributions’ payments

Traditional advertising contributions will be payable twice a year – by 25 July (an advance contribution for the first half of the year) and the annual contribution paid by January 25 of the following year.

Internet advertising contributions will be payable for annual billing periods by 25 February of the following year. The entities obliged to pay advertisement contributions will also have to submit declarations of contributions on the date of their payment. The competent authority in matters relating to the advertisement contributions will be the Head of the Second Silesian Tax Office in Bielsko-Biała.

The draft act is to enter into force on 1 July 2021, with the obligation to settle advertising fee for the period from the effective date of the act until 31 December 2021. The draft act is currently in the public consultation phase (until 16 February 2021) and may still be amended. The act may also eventually not be adopted.